Why it is important to declare your crypto currency on your income tax return.

Introduction: Why crypto tax compliance matters

South Africa’s regulatory landscape has matured rapidly since the first public warnings about crypto‑assets in 2014. Today, the South African Revenue Service (SARS) treats cryptocurrencies as crypto assets—digital representations of value that are not issued by a central bank and that rely on cryptography. In 2026, normal income‑tax rules apply to crypto assets; taxpayers must declare gains or losses on their returns. Failure to report crypto transactions can lead to interest, penalties, or even criminal charges. As regulators adopt the OECD’s Crypto‑Asset Reporting Framework (CARF), the window for “invisible” trading is closing. This guide—written for clients of Admin Boss—explains how crypto is taxed in South Africa, the new reporting rules, and how to structure your tax record keeping. It also provides search‑engine‑optimised structure and schema recommendations that align with Google’s 2026 core updates.

Understanding South Africa’s crypto‑asset tax landscape

What qualifies as a crypto asset?

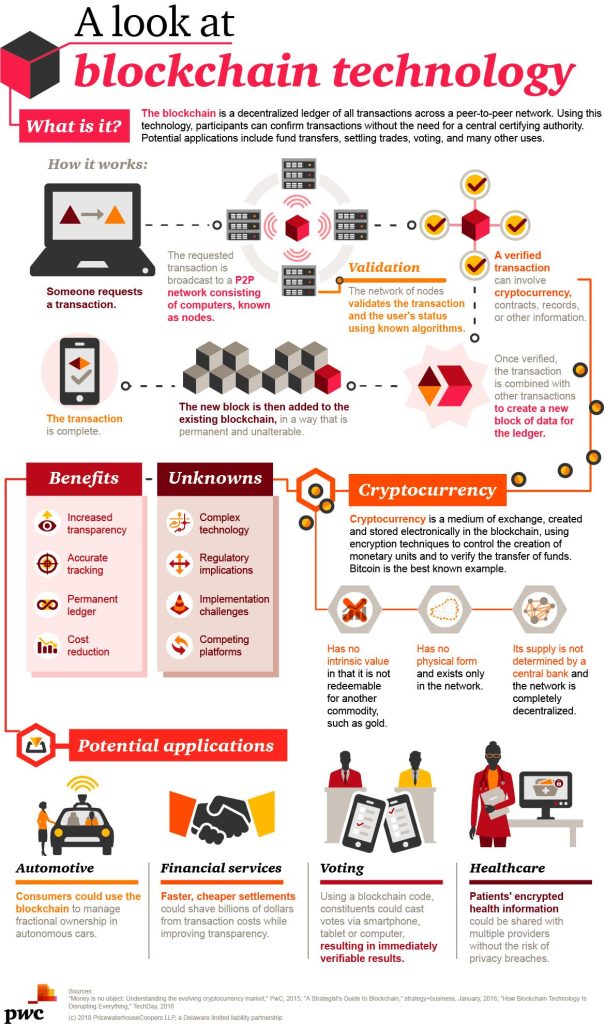

South African legislation replaced the term “cryptocurrency” with crypto asset in 2021, reflecting international consistency. SARS defines a crypto asset as a digital representation of value that is not issued by a central bank and is traded, transferred and stored electronically by individuals or legal entities. This broad definition covers Bitcoin, Ethereum, stablecoins, non‑fungible tokens (NFTs) and emerging DeFi tokens.

How did we get here?

- 2014–2016 – early warnings and the Intergovernmental FinTech Working Group (IFWG): National Treasury, SARB, the Financial Sector Conduct Authority (FSCA) and SARS issued public statements warning about crypto risks and formed the IFWG. The group fosters fintech innovation and studies the risks and benefits of crypto.

- 2018–2021 – consultation and position papers: SARS published a media release clarifying the tax treatment of crypto currencies, a list of FAQs, and collaborated on IFWG consultation papers and position papers.

- 2024–2026 – regulatory tightening: SARS continues to work with global bodies. Draft CARF regulations will make third‑party reporting mandatory from 1 March 2026. Service providers will have to report detailed transaction information to SARS.

Why crypto assets are taxable

SARS regards crypto assets as property, not currency. Normal income tax rules apply. Broadly, gains or losses from crypto transactions can be taxed as:

- Income (Revenue account) – If you trade frequently, mine, stake or receive crypto as remuneration, the proceeds are added to your gross income. Mining or staking rewards, airdrops, yield farming and being paid in crypto are all income‑tax events.

- Capital gains – When you dispose of a crypto asset (sell it for fiat, swap it for another token or use it to pay for goods/services), you must calculate the difference between the cost base and the disposal price. The resulting gain or loss is subject to Capital Gains Tax (CGT). Holding (hodling) crypto does not trigger tax.

Legal obligations for taxpayers and businesses

- Onus to declare: SARS states that taxpayers must declare all crypto‑asset‑related income or losses in the tax year they are received or accrued. Failing to declare can result in interest and penalties.

- Monitoring powers: SARS collaborates with exchanges, banks and the Financial Intelligence Centre to monitor crypto transactions. Exchanges must perform Know‑Your‑Customer (KYC) checks, share data with SARS and the FIC, and report suspicious transactions. SARS can also analyse bank statements to identify crypto purchases or cash‑out transactions.

- AI and data sharing: SARS is implementing AI solutions to detect inconsistencies between tax returns and financial transactions. From 2026, CARF will require crypto‑asset service providers to report detailed customer data to SARS.

How SARS treats crypto income and capital gains

Income vs capital classification

SARS distinguishes between income (revenue) and capital transactions. The classification depends on your intention, frequency and nature of activity:

- Trading or business activity: If you trade crypto frequently or mine/stake for profit, the proceeds are included in your gross income. Trading as a business may also attract Value‑Added Tax (VAT) registration.

- Investment (capital gains): If you hold crypto as a long‑term investment and dispose of it occasionally, gains or losses are taxed under the CGT paradigm. SARS uses existing case law to determine whether an accrual is capital or revenue.

- Barter transactions: Using crypto to buy goods or services is treated as a barter transaction. The difference between the acquisition cost and the disposal value is taxable.

Scenarios that trigger tax

- Selling crypto for fiat – When you sell crypto for South African Rand or other fiat currency, you must report any gain or loss.

- Trading crypto for crypto – Swapping one crypto asset for another is a taxable disposal.

- Using crypto for goods or services – Paying for goods or services with crypto is a taxable event; the transaction is considered a disposal.

- Mining, staking and yield farming – Rewards received from mining, staking or earning yield are taxed as income.

- Crypto as remuneration or airdrops – Receiving crypto as payment or as an airdrop is income.

Expenses and deductions

Expenses incurred in generating crypto income—such as electricity and hardware costs for mining, transaction fees or professional accounting fees—may be deductible if they are incurred “in the production of income”. Under CGT, the cost base includes acquisition cost and transaction fees; base‑cost adjustments may apply.

Tax‑free events

Not every crypto activity attracts tax. According to tax specialists:

- Purchasing crypto with fiat currency does not create a tax liability until disposal.

- Simply holding crypto (hodling) does not trigger tax.

- Moving crypto between your own wallets is not taxable.

- Receiving crypto as a gift or donating crypto to a registered charity is tax‑free, although the donor may have donation tax obligations.

- Creating NFTs is not taxed until sale.

Knowing which transactions are taxable helps you avoid unnecessary declarations and allows you to plan your tax strategy.

The Crypto‑Asset Reporting Framework (CARF) and what’s changing in 2026

Global reporting rules are coming

In December 2025, SARS released draft regulations to implement the OECD Crypto‑Asset Reporting Framework (CARF). CARF aims to close the information gap that makes crypto difficult for tax authorities to track. Under CARF:

- Service providers, not taxpayers, report: Crypto‑asset service providers must collect and report detailed user data to their tax authority. Information includes your identity, tax residency, every acquisition/disposal/transfer, the rand value of each transaction and movement between wallets.

- Effective dates: CARF comes into effect 1 March 2026 with the first domestic reporting year 2026/2027. International exchanges of information begin around September 2027.

- Broad scope: Any service provider with a South African connection—tax resident, incorporated, managed or operating in SA—must report.

What this means for taxpayers

- Automatic visibility: SARS will receive detailed transaction data directly from service providers. Non‑declaration will be easily detected.

- You still have to declare: Even though providers report, taxpayers must still declare crypto gains/losses. CARF does not change the tax treatment; it improves enforcement.

- Fix non‑compliance now: If you haven’t been declaring crypto, use the Voluntary Disclosure Programme (VDP) before CARF goes live.

- Record keeping remains vital: Maintain detailed records of your transactions, valuations, wallet addresses and cost bases. SARS may question valuations or cost basis, especially for transfers between wallets.

CARF will dramatically increase transparency. Proactive compliance now reduces the risk of penalties later.

Step‑by‑step guide to preparing your crypto tax return

Proper record keeping and classification are essential. The following structured process—adapted from tax professionals—helps you prepare:

- Identify all taxable transactions – Determine all crypto transactions during the financial year (March 1–February 28/29).

- Categorise transactions – Classify each transaction as income or capital. Mining, staking, or remuneration falls under income tax; selling, trading or spending crypto triggers capital gains.

- Determine the cost base – For each asset, calculate the original purchase price. SARS generally prefers the First‑In, First‑Out (FIFO) method.

- Calculate gains, losses and income:

- Capital gains/losses – Subtract the cost base (including transaction fees) from the selling price.

- Income – Add the rand value of crypto received via mining, staking, remuneration or airdrops to your taxable income.

- Deduct expenses – Deduct transaction fees and other allowable costs.

- Report all disposals – Include details of each disposal (date, proceeds, cost base, gain/loss) on your tax return.

- Utilise capital losses – Offset future capital gains with current losses to reduce future tax bills.

- Maintain records – Keep detailed documentation (dates, amounts, market values) for at least five years; this ensures accurate reporting and protects you during audits.

If you have high‑volume or complex transactions, consider using specialised software or consulting a tax professional who understands crypto.

Common mistakes and how to avoid penalties

- Assuming anonymity: Some traders mistakenly believe crypto transactions are anonymous. SARS uses KYC data, bank transaction analysis and AI to link wallet addresses to individuals. Do not rely on privacy tools to evade tax.

- Not declaring small or loss‑making transactions: You must declare all taxable events, even if you made a loss. Non‑declaration signals non‑compliance and may trigger penalties.

- Misclassifying trading as investing: Frequent trading or staking may be treated as income, not capital. Misclassification can lead to underpaid tax.

- Poor record keeping: Incomplete or inaccurate records can result in overpayment or penalties. Keep detailed logs and consider using a crypto tax calculator.

- Ignoring new reporting obligations: CARF will give SARS full visibility. If you haven’t been compliant, engage with the VDP before 2026.

Real‑life scenario: filing crypto tax in 2026

Case study: Nomvula is a graphic designer in Johannesburg who started dabbling in crypto in 2024. In 2025 she mined Ethereum worth R5 000, bought R50 000 worth of Bitcoin which she held, swapped R10 000 of Bitcoin for Solana in January 2026, and paid a supplier 0.02 BTC in March 2026.

Classification:

- The mining reward of R5 000 is income and should be added to Nomvula’s gross income.

- The purchase of R50 000 in Bitcoin is not taxable until disposal.

- The swap of Bitcoin for Solana is a taxable disposal. Nomvula must calculate the gain or loss by subtracting the cost base of the portion of BTC disposed (using FIFO) from its rand value at the time of the swap.

- Paying the supplier counts as a barter transaction and triggers CGT.

Reporting:

Nomvula should keep detailed records of purchase prices, dates and rand values, calculate the gain/loss on the swap and payment, and include them in her 2026/27 ITR12. From March 2026, her exchange will also report these transactions to SARS under CARF. If Nomvula neglected to declare her mining income in 2024/25, she should consider using SARS’s VDP before the new rules take full effect.

Optimising your crypto tax strategy

Use losses to your advantage

Capital losses from crypto disposals can offset future capital gains. If you trade frequently, consider tax‑loss harvesting—selling underperforming assets before year‑end to realise losses, then repurchasing them later (be aware of anti‑avoidance rules). Consult a tax professional to avoid wash‑sale pitfalls.

Plan disposition dates

Timing matters. Disposing of crypto after 1 March pushes the gain into the new tax year. Align disposals with personal income thresholds to minimise your marginal tax rate. Consider splitting disposals across tax years to stay below CGT inclusion thresholds.

Claim allowable expenses

If you mine or stake, keep receipts for hardware, electricity and internet costs; they may be deductible. Always separate personal and business expenses.

Hold for long‑term capital gains

Long‑term investors (holding for over three years) may strengthen the argument that crypto is a capital asset rather than trading stock. While South African law does not provide an explicit holding‑period test, consistent long‑term holding and clear documentation support a capital classification.

Consider charitable donations and gifts

Donating crypto to a registered charity is tax‑free. Ask for a Section 18A certificate to claim a deduction. Gifting crypto does not trigger a tax event for the recipient, though the donor may need to consider donations tax.

Frequently asked questions

What is a crypto asset?

A crypto asset is a digital representation of value not issued by a central bank. It is traded and stored electronically and uses cryptography.

Do I have to declare crypto if I made a loss?

Yes. SARS requires taxpayers to declare all crypto‑related income or losses. Declaring losses can benefit you by offsetting future gains.

How does SARS know about my crypto transactions?

Exchanges must perform KYC checks, share customer data with SARS and provide transaction reports. From March 2026, CARF will require service providers to report detailed data directly to SARS. SARS also monitors bank statements for crypto‑related transfers.

Is transferring crypto between my own wallets taxable?

No. Moving crypto between wallets you control does not trigger a tax event. Tax arises when you dispose of the asset by selling, swapping or using it for goods/services.

What happens if I have not declared crypto in previous years?

With CARF on the horizon, SARS will soon have full visibility of past transactions. You should correct prior omissions through the Voluntary Disclosure Programme before penalties increase

Ready to stay compliant and protect your profits?

Admin Boss specialises in company registration, accounting and tax services tailored for South African entrepreneurs. If you’re unsure how to declare your crypto earnings or want to optimise your tax strategy, get in touch today. Our tax experts will:

- Review your crypto transactions and classify them correctly.

- Help you set up robust record‑keeping systems.

- Ensure you take full advantage of allowable deductions and losses.

- Prepare and file your return so you avoid penalties and audits.

👉 Book a free consultation now. Let Admin Boss handle the complexity while you focus on growing your portfolio. Subscribe to our newsletter for monthly tax tips and stay ahead of regulatory changes.