South Africa Individual Income Tax Guide 2026: Salaries, Commission, Rental Income, Sole Proprietors, Interest, Dividends and SARS Filing Season

South Africa Individual Income Tax Guide 2026: Salaries, Commission, Rental Income, Sole Proprietors, Interest, Dividends and SARS Filing Explained

Individual income tax in South Africa works differently depending on how income is earned. Salaries, commission income, sole proprietor earnings, rental income, dividends and investment income may all have different SARS rules.

Understanding these rules during the 2026 SARS filing season can help taxpayers avoid penalties and remain compliant.

Need SARS Tax Assistance?

Need help with tax debt, disputes or SARS compliance support?

Visit Tax Debt South AfricaTypes of Income SARS Can Tax

SARS can assess income from multiple sources. Different categories may have unique rules and filing requirements.

| Income Type | Usually Taxable | Examples |

|---|---|---|

| Salary Income | Yes | Monthly wages, bonuses, overtime |

| Commission Income | Yes | Estate agents, brokers, sales staff |

| Sole Proprietor Income | Yes | Freelancers, consultants, contractors |

| Rental Income | Yes | Residential and commercial property |

| Interest Income | Partially | Bank interest and investments |

| Dividend Income | Special Rules | Shares and investment portfolios |

Salary Income Explained

Salary income includes:

- Basic salary

- Bonuses

- Overtime

- Travel allowances

- Fringe benefits

- Commission structures

Employers generally deduct PAYE before paying employees. However, some taxpayers still need to file returns depending on their circumstances. :contentReference[oaicite:1]{index=1}

Commission Income

Commission earners frequently experience fluctuating income and tax balancing issues.

- Estate agents

- Vehicle sales staff

- Insurance brokers

- Financial advisors

Sole Proprietors

Sole proprietors remain personally responsible for tax obligations.

Typical deductible expenses:

- Internet costs

- Fuel

- Office expenses

- Marketing

- Accounting fees

Rental Income

Rental income generally forms part of taxable income.

- Rates and levies

- Maintenance

- Bond interest

- Advertising expenses

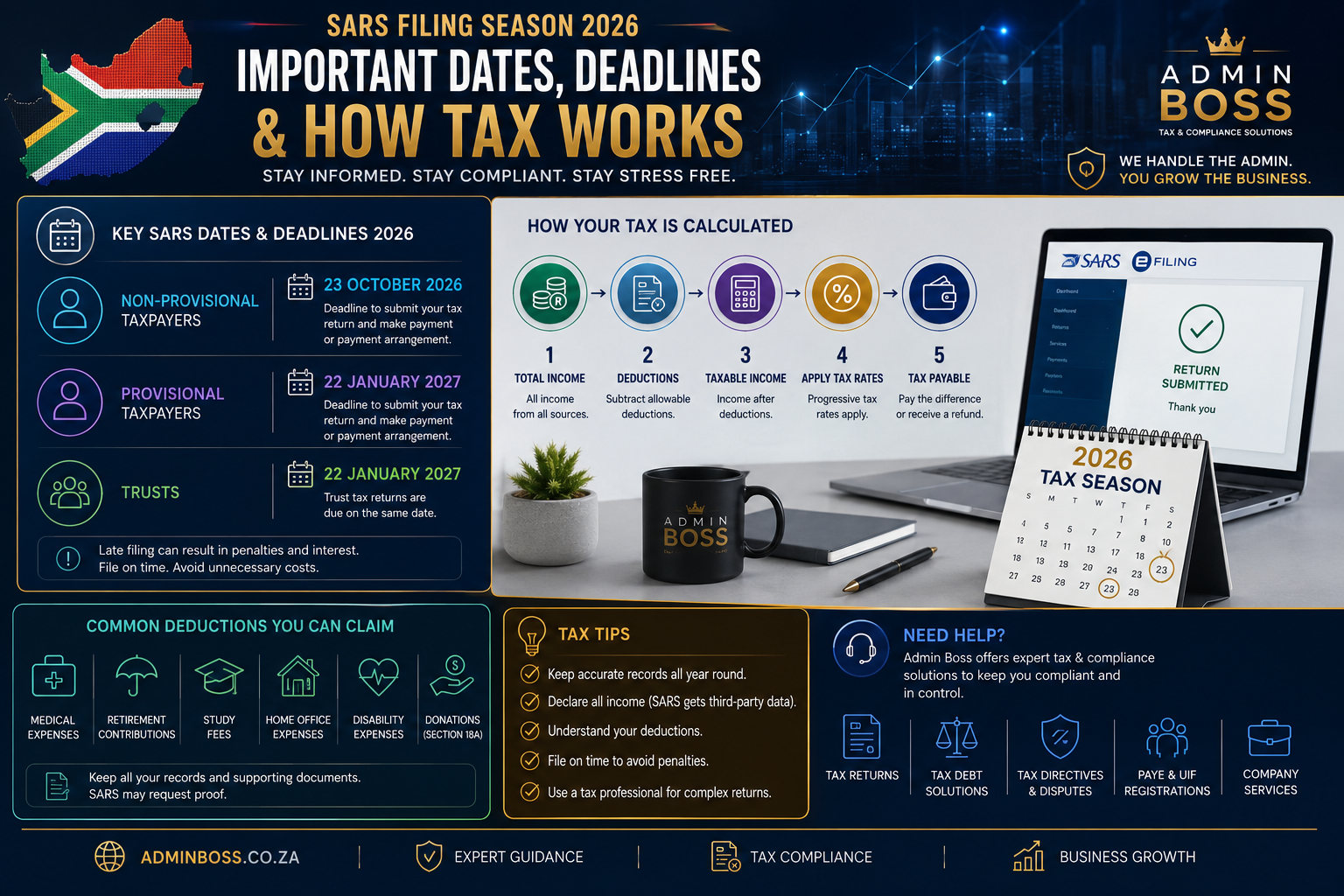

SARS Filing Season 2026

| Taxpayer Category | Deadline |

|---|---|

| Non-provisional taxpayers | 23 October 2026 |

| Provisional taxpayers | 22 January 2027 |

| Trusts | 22 January 2027 |

Published filing season deadlines indicate that non-provisional taxpayers close in October while provisional taxpayers and trusts continue into January. :contentReference[oaicite:2]{index=2}

Real Life Scenario

Meet James

James earns R25,000 per month from employment.

He also receives:

- R7,000 rental income

- R18,000 annual commission

- R11,000 bank interest

James believed PAYE covered everything. During filing season he discovered that additional earnings needed disclosure and filing updates.

After correcting his submission, he avoided penalties and improved his tax position.

Frequently Asked Questions

Do all South Africans need to submit tax returns?

No. SARS determines filing requirements based on your income and circumstances. :contentReference[oaicite:3]{index=3}

Does rental income count as taxable income?

Yes. Rental income usually forms part of total taxable income.

Can SARS see bank interest?

Banks and financial institutions submit information directly to SARS systems. :contentReference[oaicite:4]{index=4}

Does PAYE mean I never file?

Not necessarily. Additional income and deductions can still create filing requirements.

Salary Income

Description: Income earned from employment including salaries, wages, bonuses, overtime, taxable benefits and allowances.

Tax Treatment

- PAYE deducted by employer

- Personal income tax rates apply

- Additional income can still trigger filing requirements

- Multiple IRP5 certificates may require filing

Examples

- Monthly salary

- Annual bonus

- Travel allowance

- Housing allowance

Possible Deductions

- Pension fund contributions

- Retirement annuity contributions

- Provident fund contributions

- Approved donations

- Wear and tear on qualifying assets

Commission Income

Description: Income based on sales and performance earnings.

Special Rule

If commission exceeds 50% of remuneration, additional deductions may qualify.

Deductions

- Vehicle expenses

- Fuel costs

- Cellphone expenses

- Internet expenses

- Client travel

Examples

- Estate agents

- Insurance brokers

- Vehicle sales staff

Rental Income

Description: Income received from renting out residential or commercial property.

Deductible Expenses

- Bond interest

- Rates and taxes

- Advertising

- Security costs

- Levies

- Repairs

Non-Deductible

- Capital improvements

- Private expenses